#31 - DoorDash S-1; Airbnb S-1

#31 - DoorDash S-1; Airbnb S-1

Interesting nuggets from an IPO double-header

In a year already filled with star-studded IPOs, DoorDash and Airbnb are the most recent to join the fray. Here are some interesting highlights from their S-1s.

DoorDash

Market share

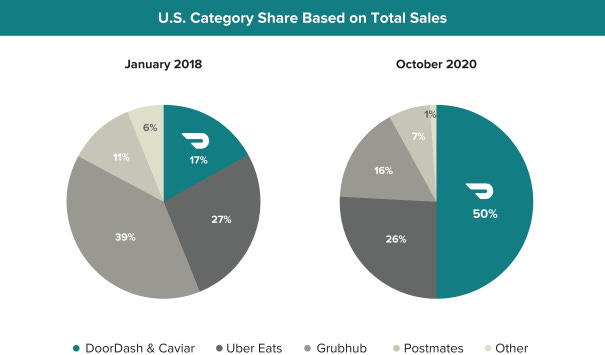

Here’s a chart from DoorDash’s S-1 that shows its remarkable growth in food delivery market share over the past two years:

And I’m not quite sure how DoorDash was able to do it! DoorDash vaguely said that its growth in market share is thanks to “the value we deliver to merchants, consumers, and Dashers,” but you need to dig elsewhere to find some clues. Here are a couple of theories that might explain the explosion in growth:

Better strategy. DoorDash has traditionally focused more on suburban markets than other food delivery companies have. This strategic focus makes sense for three reasons: (1) Suburban customers are more likely to be families who order more items per order; (2) Lighter traffic and easier parking mean that couriers can serve suburbs more efficiently; (3) Urban cities already have a lot of delivery options, so competition is fiercer. But it’s not immediately clear to me why a suburban focus would immediately result in huge growth over the past two years in entire U.S. market share. In other words, how is DoorDash leveraging dominance and experience in suburban markets to increase share in other markets?

Better operations. Maybe DoorDash just has better operational execution on increasing both restaurant supply and customer demand. With respect to restaurant supply, when DoorDash overtook Uber Eats in market share in 2019, a DoorDash spokesperson attributed its success to onboarding and partnering with restaurants faster than other delivery companies can. With respect to customer demand, according to A Balanced View, DoorDash has optimized its algorithm, learning from past data (e.g., time-of-day, repeat user behavior, pricing trends) to attract more customers. Meanwhile, competitors like Uber Eats and Postmates apparently just spray-and-pray their sales and marketing money to increase customer growth.

COVID-19 boost

In the age of deeply unprofitable tech companies going public, DoorDash actually seems pretty okay. From its S-1 (p. 93), in the 9 months ended 9/30/20, DoorDash had a net loss of $149 million on $1.916 billion of revenue, implying that DoorDash can break even if it raises revenue by ~8% while keeping costs steady. Evidence from the S-1 also suggests that DoorDash can do this! If we compare the rate of revenue increase vs. cost increase between the 9 months ended 9/30/20 with the 9 months ended 9/30/19, we’d see that DoorDash revenue grew 326% while costs grew 192% year-over-year. Perhaps DoorDash could even turn a profit in 2021 if it keeps this kind of growth up.

Of course, this is a big if and might turn on the question of whether the COVID-19 boost to food delivery is a temporary thing, or whether COVID-19 accelerated an inevitable shift to food delivery. According to the S-1, revenue exploded from $362 million in the 3 months ended 3/31/20 to $879 million for the 3 months ended 9/30/20. COVID-19 also led to an increase in working capital, from $616 million for the year ended 12/31/19 to $1.156 billion for the year ended 9/30/20. DoorDash goes so far as to explicitly call out the COVID-19 boost in its S-1: “In the second and third quarters of 2020, these trends [in increased revenue, orders, and engagement] accelerated in part due to the effects of the COVID-19 pandemic, which resulted in in-store dining shutdowns and the adoption of shelter-in-place measures.”

Logistics > Food

Here’s an interesting statistic: In its S-1, DoorDash used “food” 169 times, “logistics” 200 times, “delivery” 307 times, and “food delivery logistics” 31 times. It’s admirable how DoorDash sees itself as more than a food delivery company. Here are some more great quotes in the S-1, all from Founder Tony Xu’s Opening Letter (which, in itself, is worth reading in full):

“DoorDash has always been about helping local businesses succeed, more so than about food delivery.”

“While we started by enabling food delivery, our plan is to build products that transform the way local merchants do business and enrich the communities in which they operate.”

“We believe that by starting with food, we have created the most sophisticated and reliable logistics platform for local businesses. And, while food itself is a category that has a long runway for growth, we believe the network we have built ideally positions us to fulfill our vision of empowering all local businesses to compete in the convenience economy.”

“DoorDash is much more than an application that connects merchants, consumers, and Dashers by facilitating delivery. We provide a broad array of services that enable merchants to solve mission-critical challenges such as customer acquisition, delivery, insights and analytics, merchandising, payment processing, and customer support, and to fulfill demand generated through their own channels. This is just the beginning—we strive to become a merchant’s first call when they want to grow their business.”

I love this articulation of the vision. Perhaps one way to look at this is: DoorDash is to physical, brick-and-mortar stores what Shopify is to online stores.

It’s also interesting that at some point in each successful tech company’s lives, the mission becomes so much bigger than what it was originally. Google isn’t about search engines, it’s about organizing information. Facebook isn’t about social media, it’s about building community. Uber isn’t about ride-sharing, it’s about transportation. And DoorDash isn’t about food delivery, it’s about physical merchants. While all of these companies have built excellent products for the former, the former is only seen as a foot-in-the-door, a bottom or intermediary step to achieve the latter.

Airbnb

China

One thing that jumps out is Airbnb’s heavy emphasis on growing its share of the China market. Indeed, Airbnb devotes an entire page (pp. 53-54) outlining its risk in expanding in China. It even lists “China Growth & Quality” as a company priority that constitutes 7.5% of executive compensation.

From the S-1 (emphasis mine):

We conduct our business in China through a variable interest entity (“VIE”) and a wholly-foreign owned entity. We do not own shares in our VIE and instead rely on contractual arrangements with the equity holders of our VIE to operate our business in China because foreign investment is restricted or prohibited. Under our contractual arrangements, we must rely on the VIE and the VIE equity holders to perform their obligations in order to exercise our control over the VIE. The VIE equity holders may have conflicts of interest with us or our stockholders, and they may not act in our best interests or may not perform their obligations under these contracts. If our VIE or its equity holders fail to perform their respective obligations under the contractual arrangements, we may not be able to enforce our rights. In addition, if the Chinese government deems that the contractual arrangements in relation to our VIE do not comply with Chinese governmental restrictions on foreign investment, or if these regulations or their interpretation changes in the future, we could be subject to penalties, be forced to cease our operations in China, or be subject to restrictions in the future, and we may incur additional compliance costs. The contractual arrangements with our VIE may also be subject to scrutiny by the Chinese tax authorities and any adjustment of related party transaction pricing could lead to additional taxes.

I have two concerns about this China focus. First, I hope Airbnb will be able to place principles over profits if the two ever come in tension. Airbnb’s separate Chinese entity, Aibiying, is apparently required to share customer information such as passport numbers and guest whereabouts with Chinese authorities, storing that data in Chinese rather than U.S. servers. According to an Airbnb executive, “From the beginning, we decided what we were comfortable committing to and made that clear to Chinese authorities.” My hope is that Airbnb will transparently lay out all of its principles for operating in the Chinese market such that if Chinese authorities ever ask for more than those principles allow, Airbnb will be able to put its foot down and walk away.

Second, I’m not sure how successful Airbnb’s foray into the Chinese market will even be. Of course, the Chinese market has tempted many tech companies over the last two decades, but only a handful (Apple? Tesla? LinkedIn?) have been successful. In fact, Airbnb a few years ago was going to merge with China home sharing company Tujia, until Airbnb CEO Brian Chesky pulled the deal last-minute. In response, a Tujia executive remarked, “we will prove ourselves and show our muscle. If Airbnb needs more time to understand that they or any other foreign tech companies just can't do that well in China without a local partner, once we show them they'll sit down and talk about a deal.” The Chinese home-sharing market is starkly different from that of the West, and Airbnb, Tujia, and other companies like Xiaozhu and Meituan Duanping have been spending massively in a war of attrition to capture the market there.

Regulation

From the S-1 (emphasis mine):

We operate in approximately 100,000 cities across more than 220 countries and regions, and we are subject to various local laws and restrictions at the city, state, and country level. These laws and restrictions are dynamic. Many were instituted decades ago and did not envision Airbnb. We seek to work with governments to establish clear, fair, and workable home sharing rules to create clarity for our hosts. As of October 2019, approximately 70% of our top 200 cities by revenue before adjustments for incentives and refunds have some form of regulation.

There are two important regulations that Airbnb faces in each city:

(1) Taxes. Many cities impose relatively steep taxes on short-term lodging, hoping to obtain revenue from out-of-town travelers to spend on local residents. The most common and straightforward of these revenue raisers is a tax on traditional hotel rooms. If Airbnb expansion comes at the expense of traditional hotels, and if the apparatus for collecting taxes from Airbnb or its hosts is less well-developed than the apparatus for collecting taxes from traditional hotels, this could harm city revenues. Cities have therefore been heavily clamping down on making Airbnb pay taxes for its hosts.

(2) Zoning. The status quo of zoning regulations in cities reflects a broad presumption that short-term travelers likely impose greater externalities on long-term residents than do other long-term residents. In the case of neighbors on a street with short-term renters, these externalities include, for instance, noise and stress on neighborhood infrastructure like trash pickup. This is why hotels are typically clustered away from residential areas (e.g., Upper-West side in NYC) and in the noisier city centers (e.g., Times Square). Many Airbnb rental units are in violation of local zoning regulations, and there is the strong possibility that these units are imposing large costs on neighbors.

Note that both taxation and zoning laws apply uniformly to hotels, and Airbnb is fighting to have those laws not apply to itself. The uncharitable interpretation here is that Airbnb is engaging in a form of regulatory arbitrage and that we need to apply hotel regulations to Airbnb in order to correct a broken market. However, in my view, the more correct interpretation is that Airbnb is capitalizing on a fundamental transformation brought on by the Internet. As I wrote in California Prop 22:

[T]he Internet is predicated upon abundance and access to everyone and everything. The most transformational Internet companies are premised on this paradigm shift: On Facebook, anyone can create and share content to the world; On Amazon, anyone can create and sell products to the world; On Google, anyone can search for anything in the world. And, on Uber, anyone should be able to become a driver.

And similarly, anyone on Airbnb should be able to become a host. Imposing hotel regulations would seriously increase the barriers for people with entrepreneurial drive trying to make livings off of running their own mini, ad hoc quasi-hotel chains.

To be clear, though, I’m not saying that Airbnb should skirt all regulation. Indeed, Airbnb does create some negative consequences, like, for instance, increasing the cost of local housing and long-term rentals. However, blindly applying pre-Internet regulation to post-Internet companies is kinda’ like trying to fit a square peg in a round hole. The Internet is fundamentally different from what came before, and we need to ask ourselves how regulation should adapt to reflect this new reality.

📚What I’m reading

A bunch of these articles aren’t current but are related to DoorDash / Airbnb:

DoorDash and pizza arbitrage. DoorDash growth hasn’t come without some really bad (and hilarious) snafus.

Four strategies to win big with low frequency marketplaces. Casey Winters, current CPO at Eventbrite, wrote a post a while ago comparing customer acquisition strategies among low-frequency marketplaces like Expedia and Airbnb.

Subject: Airbnb. Back in March 2011, Paul Graham revealed a fascinating story about Airbnb and a possible investment from Union Square Ventures VC Fred Wilson.

Dashing to IPO. Alex Taussig, a VC a Lightspeed, does a deep dive into DoorDash’s IPO (far deeper than mine).

How Domino’s Pizza succeeded by acting like a tech startup.

Uber in talks to sell self-driving unit to Aurora. I’ve been questioning Uber’s focus on self-driving cars for about 3 years now. In the self-driving ride-hailing value chain, I’m not sure that all, or even the majority, of the value will accrue to the players that own the car (e.g., Google’s Waymo). I think a lot of value will also accrue to whoever owns the network (e.g., Uber, Lyft). To the extent that Uber’s self-driving unit diverted focus on improving the network, the foray into self-driving may have been a bad move. It may be smarter to simply partner with the self-driving car companies, as Lyft did with Google.

How do you know when society is about to fall apart?

To own or not to own delivery?

One big challenge for Biden? China’s push for tech supremacy. From the article: “Those on both sides of the political divide increasingly agree that a more assertive approach towards China is needed. Years of policies aimed at encouraging China to open its market, change its policies on technology transfer, and abide by international norms on human rights have apparently failed. Even so, there is a consensus among many experienced China hands that the US needs to be more strategic.”